Broker Approval

Before or After 1st Submission

Broker Portal

Submit & Manage Loan

Full Pricer

Sign-Up

/

Login

Quick Pricer

Quick Guide

Quick Submit

Niches

Rates

Matrices

Guidelines

Forms

About

Contact

Previous

Next

Lending States (Red States)

TRID (Non-DSCR)

DSCR (Non-TRID)

Programs

B - Exclusive Non-QM Alt-A

B - Exclusive Non-QM Non-Prime

B - Exclusive Investor No Stated Income

B2 - 3.99% Investor No Stated Income

Doc Types

Programs

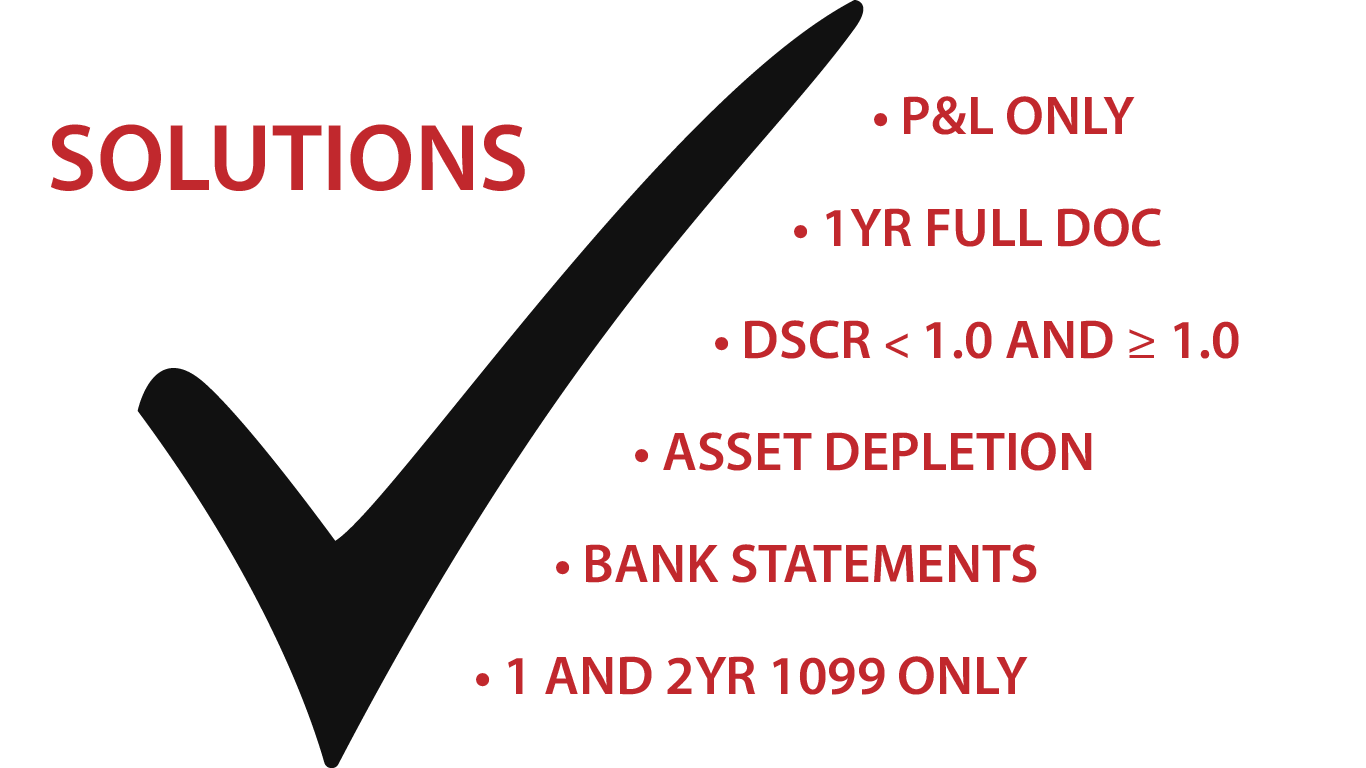

1&2 Yr Full, 12&24 Mo Bk Stmt, Asset Dep, 1099 Only

B

1&2 Yr Full, 12&24 Mo Bk Stmt, Asset Dep, 1099 Only

B

DSCR < 1.0 and DSCR >= 1.0

B

DSCR >= 0.750

B2

Find Out More About SOLVE

×

Please complete if you would like to be contacted by an Account Executive.

Email:

Phone:

Contact Me